Why engage with issuers?

Neuberger Berman believes that engagement is a dialogue between investors and companies focused on positively influencing corporate behaviors to drive long-term, sustainable returns for our clients. As a multi-asset class manager we engage with issuers across the capital structure using a range of tools and formal and informal approaches.

Our engagement efforts are particularly important in non-investment grade credit where issuers have less balance sheet flexibility to absorb unexpected deterioration in their businesses due to material environmental, social and governance (ESG) risks. We believe that maintaining an active dialogue with senior management is an essential driver of consistent long-term investment results, as it provides us with a more holistic understanding of the credit risk, enables us to offer feedback when we see shortcomings, and allows us to suggest alternative steps to protect value when necessary.

Investors have historically thought of equity investors as taking the lead role in terms of engagement, yet many high yield issuers are closely held or private businesses that are less exposed to the influence of proxy voting because of their limited equity floats. These issuers are often reliant on the fixed income markets to grow and sustain their businesses, putting non-investment grade credit investors in a position of significant responsibility and influence when an issuer comes to market seeking to finance or refinance existing debt.

With this in mind we embed active engagement in the heart of our investment process. This work is led by our experienced credit analysts, not by a separate engagement team, allowing the analyst to engage holistically with an issuer on business fundamentals, capital structure, cash flow priorities, and material environmental, social and governance issues.

We formally and systematically assess material ESG factors for each issuer as part of our investment process, using a non-investment grade credit specific governance assessment and our own environmental and social assessment, which was informed by the work of the Sustainability Accounting Standards Board (SASB). This assessment directly impacts our willingness to purchase a credit and helps identify areas for engagement both prior to and after a credit is purchased.

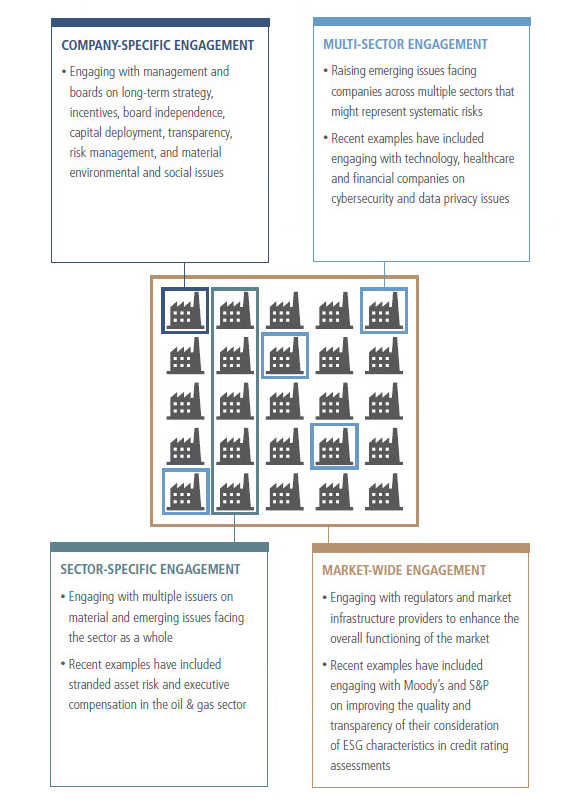

We Engage at Multiple Levels to Enhance Value and Improve Market Functionality

Our engagement efforts are not limited to just company-specific discussions; we also engage at the sector level and across multiple sectors on cross-cutting thematic risks. This helps us create value for our clients by better assessing and pricing systematic risk, as well as understanding the potential vulnerability of issuers to contagion from negative perceptions of other issuers.

We also engage at the market level to enhance overall market functionality. These broader engagement efforts are often collaborative and focused on enhanced disclosure. For example, we have been working since 2016 with the UNsupported PRI to engage credit rating agencies like Moody’s and S&P on the importance of consistent, transparent and evidenced reviews of material ESG risks as part of their credit rating assessments. We see the credit rating agencies as an important lever to encourage issuers to improve their disclosure practices, potentially reducing borrowing costs for ESG leaders and enhancing our ability to create value for our clients.

“Management trustworthiness and good governance are large factors in our investment thesis and can serve as both positive and negative overlays to our broader assessment. In addition to the scrutiny applied by the analysts, these topics are discussed by a Credit Committee comprised of the firm’s senior portfolio managers, analysts and experts who deliberatively challenge underlying assumptions and help ground the debate.”

—Chris Kocinski

Engagement in Practice: Pharmaceuticals Case Study

Background and Context

Another dimension of our engagement starts when companies originally come to market to raise capital. An issuer in the pharmaceutical industry was seeking to engage leading up to the potential financing of M&A activity. We engaged with management, first in a broad investor setting, and subsequently with focused discussions. Our initial aim during these types of engagements is to gather enough information about the company and the management team to form an accurate picture of material risks at the company. Reviewing material ESG issues, like drug pricing and ethical practices, and assessing governance considerations in our proprietary Management Scorecard are important parts of our valuation determinations.

Engagement with Management

The company had attractive cash flows, but during our discussions we developed concerns about the sensitivity of its product portfolio to certain social risks related to public perceptions of drug pricing strategies. Specifically, we closely follow the regulatory environment and saw material headline risk that could prompt regulatory action and substantially jeopardize management’s growth strategy. Other issuers were facing high-profile media attention for similar practices and we weren’t sure if the company was sufficiently adding value to the underlying products to justify the significant markups. We factored this into the Management Scorecard which, with our evaluation using our proprietary Credit Best Practices framework, influenced the decision to pass on the investment.

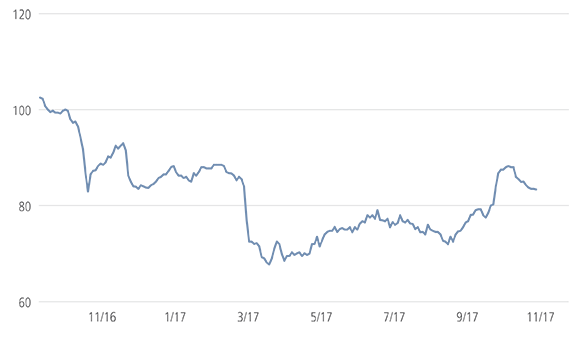

9% Senior Secured Notes - Declined New Issue on 10/6/16

9.5% Senior Unsecured Notes - Declined New Issue on 10/19/15

Source: Bloomberg.

Subsequent Action and Outcome

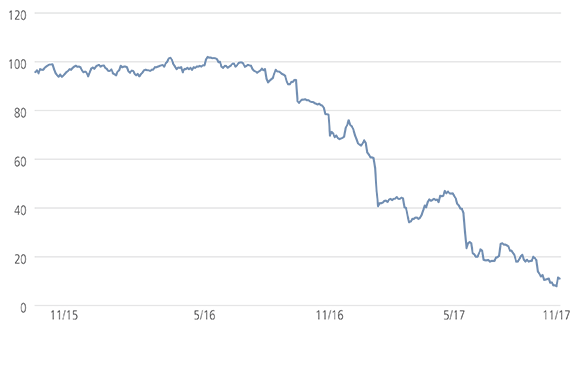

We continued to monitor the company as a potential investment, and approximately a year later, we revisited our assessment. During the engagement with the company, we discussed the reasons we had previously passed on the investment opportunity. On the topic of portfolio quality, management was still unable to placate our concerns about pressures on drug prices and the growing public scrutiny of pricing practices. The company’s balance sheet was low on tangible assets and its R&D spending would, in our view, not be able to sustain the company for the long term. We grounded our assessment of the various global legislative risks by consulting experts on the issue, and decided that we were unable to accurately model such a material risk to our investment consideration. Because of these factors, we once again declined the opportunity to invest, and flagged the concerns for the broader firm-wide investment platform.

As the increased international focus on drug pricing persisted, the company’s cash flows came under increasing pressure, leading to material increases in leverage. This, in turn, led to a further deterioration of the trading levels of the company’s high yield bonds and leveraged loans. In our view the company lacked sufficient focus on innovation and the ability to develop new products that would, over the long term, support this capital structure. As a result, the company is now in discussions to restructure their debt through a bankruptcy process. Our focus on material ESG issues allowed us to avoid this credit deterioration and to protect value for our investors.

Engagement in Practice: Oil & Gas Case Study

Background and Context

In a recent example of company-specific engagement, an analyst identified a material deficiency in disclosure practices of an issuer. The characteristics of contractual cash flows within the non-investment grade credit gas distribution sector are an important component of the credit analysis process. The issuer had disclosed that a recently acquired entity benefitted from stable take-or-pay contractual cash flows, but we found the disclosure to be vague, which in our view put future cash flows associated with the contract at risk. We were concerned that any increase in volatility in the commodity market might be associated with risks beyond those disclosed. To more fully understand the potential risk to the investment, we engaged with senior management to seek additional clarity.

Engagement with Management

In addition to helping us understand and assess risk related to a particular contract, the engagement served to determine whether the disclosure deficiency was an indicator of broader governance issues. Specifically, we sought to understand the process the company used in its due diligence, what controls and oversight existed, and how appropriate disclosure was determined and communicated to the public.

We met with senior management of the issuer on several occasions to express our concerns and to encourage improvements. Our dialogue with the CEO of the company focused on the disclosures provided for the contract in question, and we asked that additional clarification be publicly released so that investors can conduct a more complete analysis. As the commodity environment deteriorated, the risk was rising and the issuer subsequently filed additional disclosures, indicating that the contract could be at risk in certain circumstances, and that the cash flows derived under the contract were not as stable as originally communicated to investors.

We maintained our dialogue and communicated our dissatisfaction with the pattern of disclosures on this key issue. We also expressed our concerns that this situation was emblematic of a governance and oversight shortfall and needed to be addressed at the board level as soon as possible. This was chiefly rooted in our concern that adequate controls to assess acquisitions were not in place and that the presence of this issue showed that the right questions were not being asked. During an in-person follow-up meeting with the CEO, we further discussed these concerns as well as overall capital allocation and fundamental business issues.

The company’s board evidently developed its own concerns and several members of management were dismissed before we could conclude our engagement on this issue. Given these developments, we subsequently scheduled a meeting with the chairman of the company with the goal of continuing dialogue. We again expressed dissatisfaction with the pattern of disclosure on the key contract described above and encouraged change within the organization to re-focus the business and improve visibility for investors. This was also an opportunity for us to provide a market-level perspective on what we observe to be best practices of management communications and opportunities for improvement for the company.

Subsequent Action and Outcome

In our opinion, our engagement with the issuer resulted in improved transparency for investors and allowed us to make better informed decisions for our clients. This allowed us to make a more in-depth assessment of this investment, ultimately deciding not to exit the position at that time. Clarity achieved on the contractual cash flows and capital allocation decisions were drivers of our decision to increase our position in the issuer during this period of trading volatility.

As the market gained greater clarity on management’s capital allocation decisions and the contract in question we continued to actively monitor the issuer’s credit profile and engaged with the management team on key topics related to the business and disclosure practices. Ultimately we determined the company was not sufficiently proactive in addressing our concerns about high levels of leverage and liquidity and when they were unable to meet our expectations of significantly improved corporate governance we made the decision to exit the position. We believe that this case study exemplifies the importance of ongoing management engagement in our assessment of management quality. The credibility developed by being a long-term and active lender can provide a platform to influence change, which can lead to better informed decisions and enhance long-term investment performance.

“Analyzing ESG characteristics enhances traditional credit analysis by providing a fuller understanding of the risk profile of each issuer. Our proprietary credit analysis frameworks integrate bottom-up ESG research in order to enable our portfolio managers to better assess investment opportunities. Portfolio managers can also use ESG characteristics as an additional differentiator on a risk-adjusted basis during portfolio construction.”

Neuberger Berman ESG Policy