In a rising interest rate environment, the case for senior floating rate loans should be revisited. Indeed, we believe this asset class deserves a strategic allocation in an investor’s portfolio. In our opinion, senior loans have the following qualities:

- Attractive yield potential – Their yield was among the highest of all fixed income asset classes (as of December 2016).

- Protection against duration risk – They have very low duration and the coupons adjust regularly based on the London Inter Bank Offered Rate (LIBOR).

- Protection against credit risk – They are typically secured and their senior positioning in the capital structure offers protection relative to High Yield bonds.

- Low correlation to other asset classes – They historically have outperformed the broader fixed income market in flat and rising rate environments. They typically have a low correlation to other fixed income asset classes and we believe loans can provide diversification benefits in investor portfolios.

Senior floating rate loans provide a unique combination of relatively high income potential and low duration thanks to their floating rate coupon. In addition, the senior secured nature of the loans mitigates the credit risk as their seniority creates lower expected losses compared to other non-investment grade assets.

Their lower correlation to other major asset classes also provides diversification and reduces a portfolio’s overall risk when compared to instruments with higher sensitivity to interest rates. And senior floating rate loans have historically provided investors with lower volatility compared to other risky and long-duration assets as well.

Senior Floating Rate Loans: A Primer

Generally arranged by banks on behalf of businesses and then sold to institutional investors, these loans typically back recapitalizations, acquisitions, refinancings, leveraged buyouts, capital expenditures and other general corporate purposes. They are typically the most senior debt position within the borrowing firm’s capital structure, which means they would be the first to be paid back in the event of default. Many of these borrowers are household names (e.g., United Airlines, Goodyear Tire and Hilton Hotels), and the market contains more than 1,000 issuers and over 30 different sectors, making up about $900 billion in par value.

There is an active secondary market for the loans, with over $2 billion of average trading volume per day, and a wide range of participation from institutional investors. Collateralized Loan Obligations, or CLOs, are the largest buyers of loans, although investor diversity has increased over the past 10 years. Retail mutual funds, for example, now hold around 20% of all loans outstanding.

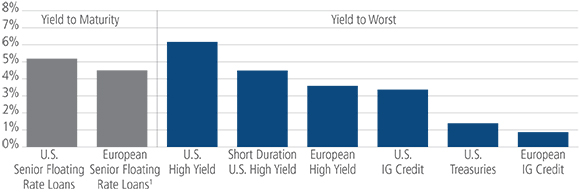

1. Attractive yields

The yields from floating rate loans are typically among the highest of all fixed income asset classes. As of December 2016, U.S. loans, for example, have yielded 5.4% according to Bloomberg, just shy of U.S. High Yield and significantly higher than overnment bonds and Investment Grade Corporates. Given the low yield environment around the globe, a higher income-producing investment could be attractive to a diverse set of investors.

Asset Class Yield Comparison1

Source: S&P Capital IQ LCD & Bank of America Merrill Lynch.

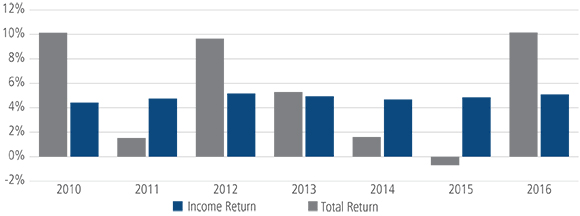

The income component of the senior loan total return has historically provided stability to overall returns. Indeed, the significant regular distributions help to dampen any potential mark-to-market volatility on the underlying loan prices.

Total Return Composition1

Source: S&P Capital IQ.

2. Protection against a rising rate environment

The coupons on floating rate loans generally reset every 30 to 90 days, and the reset is based on the prevailing LIBOR rate at that time. Given the coupons are reset in very short intervals, based on 1- or 3-month LIBOR, means that floating rate loans have near zero duration. And, as an added benefit, as LIBOR rises, so does the coupon paid on the underlying loan, increasing the income to investors.

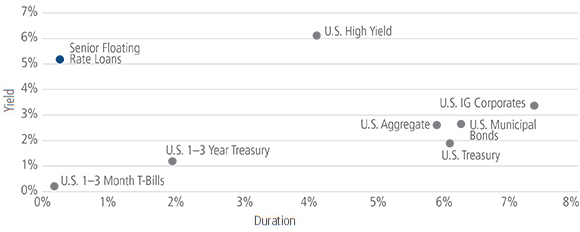

As you can see below, when you combine the historical yields on loans with the low duration, the result is the highest ratio of yield per unit of duration versus other major fixed income asset classes.

Yield Versus Duration1

Source: FactSet, Barclays POINT. Past performance is not necessarily indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss.

In addition, when we look at the last five periods of rising rates since 1999, the performance of loans versus bonds highlights their relative stability and outperformance compared to other fixed income asset classes. The relative outperformance is particularly acute when compared to government bonds.

Loan Performance in Rising Rate Environment

Source: J.P.Morgan.

3. Protection against credit risk

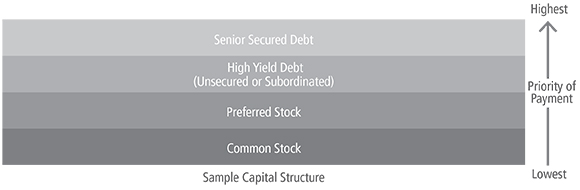

The senior secured positioning that loans hold on the capital structure can help reduce credit risk to investors, which other investments typically do not provide. Loan investors receive priority for repayment in the event of a default over other obligations, and before stock or bond holders. Loans also hold a first priority line on the assets of the borrower, including cash receivables, inventory and property, and plant and equipment.

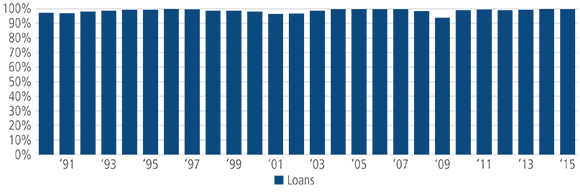

Over the past 15 years, the average recovery rate on loans that default is 70%, meaning that credit losses amount to 30% of the 3% average annual default rate, or about 1%. This implies that 99% of principal has been returned to investors over a period that has included a number of recessions, which means almost all the annual income that is generated from a portfolio of loans is retained by investors (See Figure 6).

Capital Preservation

Source: Moody’s Investors Service report February 2016.

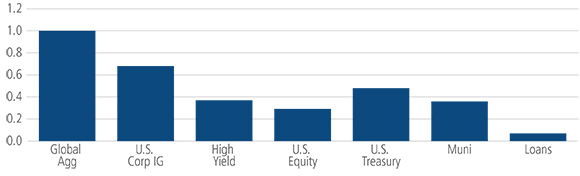

4. Low correlation to other asset classes

Given their floating rate coupon, loans have historically offered a low correlation to the Global Aggregate, which is a longer duration asset class, as the chart below highlights.

Source: Bloomberg, Barclays.

Given the significant bull market in fixed income over the past 20 years, fixed rate, long duration instruments have performed extremely well. For the 20 years ended December 2016, the yield on 10-year U.S. Treasury fell from 6.3% to 1.8%*. This was an incredible boost for traditional bonds as declining rates pushed up their prices and enhanced total return. This clearly made traditional bonds look more attractive than loans, whose prices are generally unaffected by interest rate changes, from both a return and a Sharpe Ratio perspective—see chart below.

Returns by asset class, January 1997 to October 2016

| Annualized Returns | Standard Deviation of Monthly Returns | Sharpe Ratio | |

|---|---|---|---|

| S&P/LSTA Index | 5.19% | 1.72% | 0.47 |

| BAML HY Master (H0A0) | 7.39% | 2.63% | 0.55 |

| 10-year Treasury (GA10) | 5.58% | 2.12% | 0.43 |

| S&P 500, including dividends (SPX) | 8.49% | 4.42% | 0.40 |

| BAML High-Grade Corp. (C0A0) | 6.20% | 1.53% | 0.72 |

Source: LCD, an offering of S&P Global Market Intelligence, Bank of America Merrill Lynch

However, as we reach an inflection point in interest rates, we believe loans could be poised to outperform over the years to come. The lower volatility of the loan asset class has been clearly demonstrated and can be seen above in the standard deviation of monthly returns. In short, we believe that the Sharpe Ratio should improve over the coming years as the tailwind from declining interest rates starts to wane.

Conclusion

Since it is difficult to predict exactly when interest rates will rise, or their path, we believe the embedded benefits of the loan asset class make a compelling case for a strategic allocation. These positive attributes, which include relatively high current yields, duration and credit protection, as well as a low correlation to other fixed income options, mean a permanent allocation to loans can provide benefits in any market environment.