While these questions are relevant for any marketplace, they are currently being used to analyze how retirement plan participants make investment decisions. And the answers are driving some significant changes in how plan sponsors construct investment menus.

Studies demonstrate that too many investment choices can overwhelm participants with limited investment expertise, causing them to disengage and not participate in the plan.1 To simplify the investment decision-making process for these participants, many plan sponsors have opted to default them into a target date fund (TDF). A recent study revealed that TDFs are available in more than 70% of plans, with 35% of the account balances of newly hired participants invested in TDFs.2

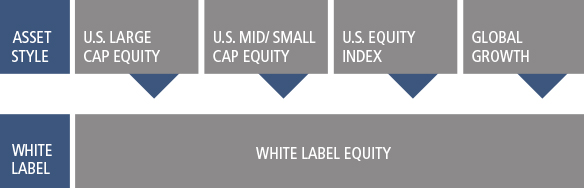

Another investment simplification strategy that is attracting growing interest is “white label funds.” White label funds are generically named funds that are branded by their asset class or objective, rather than by reference to a particular fund company. Unlike the TDF, which groups all employees with a common anticipated retirement date into the same fund, white labeling is designed to help participants make more informed investment choices tailored to their individual needs and objectives. Descriptive titles are assigned to each white label fund to make the underlying investment objectives easier for participants to understand. It is also common to consolidate multiple investment options into a single white label fund. This reduces the number of investment options, further simplifying choices for participants who lack investment expertise.

White labeling is now used by 24% of large plans.3 With many retirement plan trends, what starts with large plans often moves down market to mid-size and smaller plans. Given technology innovations and growing awareness, this may well be the case with white label funds.

This article will explore some of the factors that are driving a growing number of financial advisors and plan sponsors to conclude that white label funds provide an effective balance of meaningful investment information and a reasonable number of options. We will also highlight some of the challenges in working with white label funds that you may want to discuss with your plan sponsor clients when analyzing whether this option is a good fit for their plan.

More Is Not Always Better

Plan sponsors have a fiduciary obligation to prudently select a menu of investment options for a participant-directed plan such as a 401(k) plan.4 The investment options must be sufficiently diversified to avoid the risk of large losses.4 Plan sponsors often struggle with the question of how many investment options are needed to create a menu that is diversified and fits a wide variety of participant needs. Plan sponsors have increasingly arrived at the answer that “more is better.”5

The trend toward broadening investment menus was likely motivated by plan sponsors’ desire to increase participant satisfaction and participation rates by offering the variety and brand preferences participants wanted. Unfortunately, it has had the opposite effect.

A study conducted by Columbia Business School professors found that as the number of investment options increased, employee participation rates dropped. For every 10 investment options offered:

- Participation rates dropped by 1.5% – 2%.

- Allocations to equity funds dropped by over 3% and allocations to money market and bond funds increased by about 4%.

- The number of participants who contributed nothing to equity funds rose by about 3%.1

While the types of funds that experienced increased use were certainly appropriate for some participants, the study found they were not the optimal choice for all participants, especially those seeking to maximize their retirement savings.

Titles May Not Tell the Whole Story

Just as too many choices can lead to bad outcomes in the form of reduced participation rates, not understanding the options can also lead to negative participant outcomes. Participants without investment experience may recognize the name of the fund providers, but not understand the funds’ objectives. Names such as ABC Aggressive Growth Fund, DEF International Allocation Fund and XYZ Total Return Fund mean something to financial advisors, but may not mean anything to participants. In some cases, this can lead to participants who are overwhelmed or confused and then choose not to participate in the plan or who then make inappropriate investment choices. One study indicated that 57% of plans that used a white label fund alternative felt the strategy helped simplify participant communications and made investment options easier for participants to understand.3

Why and How to Construct a White Label Alternative

The white label strategy has been used to simplify the investment selection process for participants both in terms of reducing the number of investment options and making the investment objectives of each option more understandable and meaningful for participants. White labeling can be applied in different ways:

- Retitle individual investment options—In some cases, existing investment options are simply retitled with a more descriptive label, such as U.S. Stock fund or U.S. Bond fund, to make it easier for participants to understand what the investment objectives are and how the fund is investing their retirement dollars.

- Combine multiple investment options—Most commonly, multiple investment options are combined under the more descriptive name. This often involves combining what are stand-alone investments based on asset classes in the current investment menu into a single investment option. For example, instead of having a global equity, small cap, large cap, and an equity index fund, they are combined into a single equity option. Incorporating multiple investments into one white label has the added advantage of reducing the number of investment alternatives.

- Construct from core investment options—Some plans construct white label funds using a mix of core investment alternatives already available to participants in the plan.

- Include investments not in core menu—Some plans use a combination of investments from the plan’s current menu that will not be offered as stand-alone investment options and are only available as a component of a white label fund. This option is sometimes used when an investment option standing on its own may not be deemed prudent for participants, or has the potential to be misused, but may be appropriate as a component of a diversified investment vehicle. The increased diversification this method offers can be attractive to plan fiduciaries.

Access to White Label Services

Studies that evaluate the use of white label funds have generally focused on large plan adoption rates. As more retirement plan service providers, such as recordkeepers, are able to provide the services needed to support this option, it may become more available and more appealing to mid-size and smaller plans.

Today, advisors still have options for simplifying investments for their smaller plan clients. Many recordkeepers and other service providers provide the tools to enable advisors to build investment “models” or plan-level “advisor managed accounts” based on the investment options available in the plan. These services are provided across a broad spectrum of plan sizes. These “fund of fund” options enable advisors to deliver an experience with a similar objective to white label funds today, to plans of any size.

As you are evaluating the potential addition of white label services or expanding your managed account services as part of your business model, be sure to consult with your firm’s legal and compliance resources to confirm your proposed services are in compliance with your firm’s policies and procedures. Given the potential ERISA fiduciary role advisors take on when providing white label services, you will likely need to review service agreements and disclosures. Your firm may also have preferred tools or third party service providers that you can tap into when offering white label services to plan sponsor clients.

Weighing the Options

As with any retirement plan decision, there is no one-size-fits-all solution. Each plan sponsor must follow an investment selection due diligence process in analyzing whether it is prudent to offer white label funds. Most plans adopt an investment policy statement (IPS) to guide their investment decisions. Be sure to consult the IPS as you discuss the investment strategies. Following are some additional issues that you may want to discuss with plan sponsors considering a white label strategy.

Potential Benefits

Simpler, more understandable options for participants

|

Increased investment diversification

|

Cost savings

|

Flexibility

|

Considerations

Complexity

|

Participant reporting and communication challenges

|

Costs

|

Financial Advisor Support

As you explore options for improving participant retirement savings outcomes, white label funds may be of interest to some of your plan sponsor clients and prospective clients, especially for larger plans. As an advisor, you play a crucial role helping plan sponsors evaluate the white label option.

Clients will need your support to:

- Learn about the role of a white label option in an investment menu

- Execute an investment selection due diligence process to evaluate whether to add white label funds

- Evaluate service providers to administer the white label services and provide participant communications

- Explore options regarding how to construct the white label funds

- Monitor investment performance of the white label funds and each underlying investment